Life insurance is an essential financial tool that provides security and peace of mind by protecting your loved ones against financial hardship in the event of your death. When seeking life insurance, one of the most important considerations is the cost of your premium, which is the regular payment you make to keep the policy active. This cost is typically expressed through life insurance quotes, which can vary greatly depending on numerous factors.

Understanding what influences your life insurance quote is vital because it allows you to make informed decisions, choose the right policy, and potentially save money. This article explores in detail the many factors insurers consider when calculating your life insurance premium.

Key Takeaways

- Age and health are the biggest drivers of your life insurance premium.

- Women typically pay lower premiums than men due to longer life expectancy.

- Smoking and hazardous hobbies increase your premium substantially.

- The type of policy and coverage amount you choose significantly affect your cost.

- Shopping around and maintaining a healthy lifestyle can help you secure better rates.

- Honest disclosure of your medical and lifestyle information is critical.

- Buying life insurance earlier in life usually results in lower premiums and better coverage options.

What is a Life Insurance Quote?

Life insurance companies don’t just assign prices randomly. Instead, they use complex statistical methods, historical data, and underwriting techniques to calculate your risk profile. The risk profile reflects the insurer’s assessment of how likely you are to pass away during the coverage period, which directly influences how much you will pay.

To generate a quote, insurers analyze several aspects of your personal and health information:

- Age: Younger people tend to get lower quotes because they are less likely to die soon.

- Gender: Statistically, women live longer than men, often leading to lower premiums.

- Health status: Pre-existing conditions, current medical treatments, and lifestyle habits (like smoking) affect risk.

- Family medical history: Genetic predispositions to illnesses can increase premiums.

- Occupation and hobbies: Risky jobs and activities may lead to higher quotes.

- Policy details: The amount of coverage and length of the policy term also influence the quote.

Role of Actuarial Data

Insurance companies rely heavily on actuarial data — statistical data collected from large groups of people over many years. Actuaries analyze this data to determine mortality rates and project the likelihood of policyholders passing away at different ages and under different circumstances. This scientific approach allows insurers to set premiums that balance their financial risk with competitive pricing.

Underwriting Process

The underwriting process is the method insurers use to evaluate an applicant’s risk level. This process often involves:

- Reviewing medical records and history.

- Conducting a medical exam (blood tests, urine tests, blood pressure measurements).

- Assessing lifestyle factors such as tobacco use, alcohol consumption, and exercise habits.

- Evaluating occupational hazards or high-risk hobbies.

Once underwriting is complete, the insurer can provide a more accurate and personalized quote based on your specific profile.

Why Do Quotes Vary Among Insurers?

Because each insurer uses slightly different actuarial tables, underwriting criteria, and risk appetites, quotes can vary widely. This is why it is recommended to shop around and compare multiple quotes to find the best deal.

How Do Life Insurance Companies Calculate Your Quote?

Understanding how life insurance companies determine your premium quote can empower you to make smarter choices and potentially lower your costs. Life insurers use a comprehensive risk assessment process to evaluate the likelihood that they will have to pay a death benefit on your policy. The goal is to set a premium that accurately reflects the risk you present as an insured individual. This underwriting process involves gathering detailed information and applying actuarial data and statistical models.

The Information Collection Process

Insurance companies collect relevant information about you through:

- Applications: You provide personal details, health history, lifestyle habits, and financial needs via application forms.

- Medical Exams: Most policies require a physical examination, blood tests, urine samples, and sometimes additional diagnostic tests. This gives insurers current, objective health data.

- Interviews: Some insurers conduct phone or in-person interviews to clarify details or better understand your lifestyle and health.

The data collected during this process forms the basis for risk evaluation.

Key Factors Insurers Analyze to Calculate Your Quote

Demographic Details

- Age: Age is one of the most significant factors. Younger applicants typically have lower premiums because they have a longer expected lifespan and pose less risk to the insurer. Premiums increase with age.

- Gender: Statistically, women live longer than men, so women often receive lower quotes.

- Location: Geographic location can influence premiums due to variations in life expectancy, healthcare quality, and environmental risks. For example, living in an area with higher pollution or fewer healthcare resources might increase premiums.

Medical History

- Current Health Status: Insurers assess your overall health, including chronic conditions like diabetes, hypertension, heart disease, or cancer. Poor health elevates risk and thus premiums.

- Past Illnesses and Surgeries: Previous serious illnesses or surgeries can signal higher risk, affecting rates.

- Medical Exam Results: Lab test results (cholesterol levels, blood sugar, kidney function) and vital signs help insurers evaluate health.

- Medications: Regular use of certain medications may indicate underlying health issues.

- Body Mass Index (BMI): Obesity or being underweight can affect life expectancy and premiums.

Family Health History

Genetics play a role in the likelihood of hereditary diseases such as heart disease, cancer, diabetes, and stroke. Insurers consider family medical history, especially in close relatives like parents and siblings, to gauge potential future health risks.

Lifestyle Choices

- Smoking: Tobacco use is one of the biggest risk factors. Smokers pay substantially higher premiums because smoking dramatically increases mortality risk.

- Alcohol Consumption: Heavy drinking can lead to liver disease and other health problems, raising premiums.

- Recreational Drug Use: Use of illegal drugs or misuse of prescription drugs often results in higher rates or policy denials.

- Diet and Exercise Habits: Healthy habits can lower risk and premiums.

- Risky Activities and Hobbies: Participation in high-risk activities like skydiving, scuba diving, or motorsports increases your risk profile.

Occupation and Travel Habits

- Occupation: Jobs with higher risks of injury or death (such as pilots, construction workers, firefighters) typically lead to higher premiums.

- Travel: Frequent travel to risky or unstable regions can affect your premium.

Financial Profile and Policy Details

- Coverage Amount: The size of the death benefit directly influences your premium. Larger coverage means more risk to the insurer.

- Policy Type: Term life insurance generally costs less than whole life or universal life policies due to different coverage structures.

- Term Length: Longer policy terms generally increase premiums because coverage extends over a longer risk period.

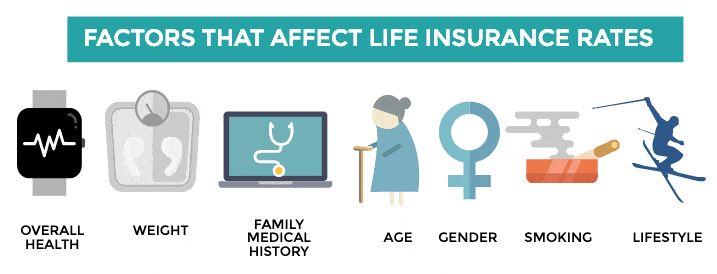

Key Factors That Affect Life Insurance Quotes

Understanding what influences your life insurance premium is crucial when shopping for the right policy. Life insurance quotes are personalized estimates that reflect your individual risk profile as assessed by the insurer. Several factors come into play during underwriting, which ultimately affect how much you will pay for coverage. Below are the most important determinants of your life insurance quote in detail:

Age

Age is one of the most critical factors in determining your life insurance premium. Insurance companies rely heavily on actuarial data, which shows that younger individuals statistically live longer and have a lower risk of death in the near term. Therefore:

- Younger applicants pay significantly lower premiums because the likelihood that the insurer will have to pay the death benefit soon is low.

- As you get older, your premium increases because the risk of health issues and mortality rises.

Example: A healthy 25-year-old applying for a 20-year term life insurance policy will pay far less than a 50-year-old applying for the same coverage. This is because the 25-year-old is expected to live much longer, making them less risky to insure.

Gender

Gender influences life insurance rates because of average life expectancy differences:

- Women generally pay lower premiums because they tend to live longer than men.

- Women are statistically less likely to experience certain life-threatening illnesses or risk-taking behaviors in early adulthood.

This longevity reduces the risk for insurers, which translates into more affordable premiums for women compared to men with the same profile.

Health and Medical History

Your present health and medical background are among the most heavily weighted factors in underwriting:

- Chronic conditions such as diabetes, hypertension, heart disease, cancer, or respiratory illnesses increase your premium significantly.

- Insurers may require a medical exam, including blood tests, urine analysis, blood pressure measurement, and possibly an EKG, to assess your overall health.

- Past surgeries, hospitalizations, and treatments are reviewed carefully.

- Obesity, high cholesterol, and other health metrics also factor into risk calculations.

A clean bill of health usually results in lower premiums, while existing or past medical issues can raise costs or even result in denial of coverage.

Lifestyle and Habits

Lifestyle choices are closely linked to mortality risk, and insurers assess these carefully:

- Smoking: Smokers typically pay two to three times higher premiums than non-smokers due to increased risks of lung cancer, heart disease, and other serious conditions.

- Alcohol consumption: Heavy or chronic drinking can raise premiums or cause coverage denial.

- Drug use: Use of recreational or illegal drugs usually leads to higher premiums or outright rejection.

- Diet and exercise: Maintaining a healthy lifestyle with good nutrition and regular exercise can positively impact your quote, often leading to reduced premiums.

By adopting healthier habits, you may improve your insurability and save money.

Occupation and Hobbies

Certain jobs and recreational activities come with increased risk, and insurers reflect this in their pricing:

- High-risk occupations such as construction workers, miners, pilots, firefighters, and law enforcement personnel face higher premiums because their jobs expose them to greater dangers.

- Risky hobbies like skydiving, scuba diving, motor racing, or extreme sports can increase your premium due to the higher likelihood of accidents or fatal injuries.

If your profession or hobbies involve risk, expect your quote to be higher or to face exclusions for those activities.

Type of Life Insurance Policy

The kind of life insurance policy you choose affects your premium:

- Term Life Insurance provides coverage for a fixed period (e.g., 10, 20, or 30 years) and generally offers the lowest premiums because it only pays out if death occurs during the term.

- Whole Life Insurance offers lifelong coverage and includes a cash value component, but premiums are significantly higher due to the permanent protection and investment element.

- Universal Life Insurance combines flexible premiums and coverage with an investment savings component, usually priced between term and whole life policies.

Choosing the right type depends on your financial goals and budget, but it will influence how much you pay.

Coverage Amount and Term Length

- The coverage amount (death benefit) directly impacts the cost. Higher coverage means the insurer assumes greater financial risk, resulting in higher premiums.

- The term length matters because longer terms mean the insurer is exposed to risk for more years, typically increasing the cost.

For example, a $500,000 policy will generally cost more than a $250,000 policy, and a 30-year term will be more expensive than a 10-year term with the same coverage amount.

Family Medical History

Your family’s health history can be a significant predictor of your own health risks:

- If immediate family members have had hereditary diseases such as heart disease, cancer, stroke, or diabetes, insurers may charge higher premiums.

- Genetic predispositions increase the likelihood of developing these conditions, increasing the insurer’s risk.

Providing detailed and honest family health information during underwriting is crucial, as it helps insurers make accurate risk assessments.

Location and Residency

Where you live can influence your life insurance premiums due to environmental and socioeconomic factors:

- Certain geographic areas have higher mortality rates based on factors like pollution, healthcare quality, crime rates, and lifestyle.

- Urban versus rural residency may also affect risk differently.

For example, someone living in an area with poor air quality or limited access to quality healthcare might pay more compared to someone in a healthier environment

How Can You Get the Best Life Insurance Quote?

Getting the best life insurance quote means not only finding an affordable premium but also securing a policy that fits your unique needs and provides adequate protection for your loved ones. Because life insurance quotes can vary widely between providers, it’s important to understand how you can optimize your application process and improve your chances of obtaining a competitive rate. Below are detailed strategies to help you get the best life insurance quote:

Maintain a Healthy Lifestyle

Your health plays a vital role in how insurers assess your risk. By adopting and maintaining healthy habits, you can positively influence your life insurance premiums:

- Regular Exercise: Engaging in consistent physical activity improves cardiovascular health, controls weight, and reduces the risk of chronic diseases such as diabetes and hypertension. Insurers view physically fit individuals as lower risk, which can translate into lower premiums.

- Balanced Diet: Eating nutritious foods rich in vitamins, minerals, and antioxidants supports overall wellness. Avoiding excessive intake of processed foods, sugars, and unhealthy fats helps maintain a healthy weight and prevents lifestyle-related illnesses.

- Avoid Tobacco: Smoking dramatically increases the risk of lung cancer, heart disease, stroke, and respiratory conditions. Smokers pay significantly higher premiums—often two to three times more than non-smokers. Quitting smoking well before applying for insurance (preferably at least 12 months) can help you qualify for non-smoker rates.

- Limit Alcohol Consumption: Excessive drinking raises the risk of liver disease, cancers, and accidents. Moderate or no alcohol use can improve your underwriting profile.

By prioritizing your health and well-being, you not only improve your quality of life but also enhance your insurability and reduce costs.

Shop Around and Compare Multiple Quotes

Life insurance premiums can vary substantially between different insurance companies due to variations in underwriting criteria and pricing models. Therefore:

- Obtain Quotes from Multiple Providers: Don’t settle for the first offer. Use online tools, insurance brokers, or agents to gather quotes from various companies.

- Compare Similar Policies: Ensure you’re comparing apples to apples by reviewing quotes for similar coverage amounts, policy types, and terms.

- Consider Reputation and Customer Service: While price matters, choose insurers with strong financial ratings and positive customer reviews to ensure reliability and smooth claims processing.

Shopping around helps you identify the best balance of coverage and cost, ensuring you don’t overpay.

Assess and Choose the Right Coverage Amount and Policy Type

Selecting a policy that matches your financial needs and budget helps avoid over-insurance or under-insurance:

- Calculate Your Coverage Needs: Consider your current debts, future financial obligations (such as children’s education), income replacement, and final expenses to determine an appropriate death benefit.

- Choose the Right Policy Type: Term life insurance usually offers the most affordable coverage for specific periods, while permanent policies like whole or universal life are costlier but provide lifelong protection and cash value components.

- Select an Appropriate Term Length: Longer terms generally cost more, so pick a duration that aligns with your financial goals (e.g., until your mortgage is paid off or children are financially independent).

Choosing thoughtfully helps optimize your premium by aligning coverage with actual needs.

Get a Medical Exam and Prepare for Underwriting

Most life insurance policies require a medical exam as part of underwriting:

- Schedule Your Exam Early: Being proactive about your medical exam lets you control the timing and prepare properly.

- Prepare Your Health: Before the exam, avoid alcohol and caffeine for at least 24 hours, get enough sleep, and stay hydrated to improve test results.

- Be Honest and Transparent: Provide accurate medical history and lifestyle details to avoid future claim denials.

- Consider No-Exam Policies if Necessary: Some insurers offer no-medical-exam policies, though these often come with higher premiums or lower coverage limits.

Good preparation can help you achieve favorable results, resulting in lower premiums.

Be Honest and Accurate on Your Application

Accurate disclosure is essential:

- Avoid Withholding Information: Concealing health conditions, tobacco use, or risky activities can lead to claim denials or policy cancellations.

- Provide Complete Information: Give full details about your medical history, medications, occupation, and lifestyle.

- Review the Application Carefully: Double-check for errors before submission.

Honesty ensures that your policy is valid and protects your beneficiaries when they need it most.

Also Read : How Do You Choose the Right Health Insurance Plan?

Conclusion

Life insurance quotes depend on a wide array of factors, with age, health, lifestyle, policy type, and coverage amount being the most influential. By understanding these factors, you can take steps to improve your health, select the right policy, and shop smartly to get the best value for your money. Life insurance remains one of the most important financial decisions you will make, and being well-informed about the determinants of your quotes will help ensure you provide the necessary protection for your loved ones.

FAQs

1. How does age affect my life insurance quote?

Premiums increase with age because the risk of mortality rises as you get older.

2. Will my premiums change if my health improves?

If your health improves significantly, some insurers allow re-evaluation and possible premium reductions.

3. Does smoking really affect life insurance quotes?

Yes, smokers typically pay significantly higher premiums due to health risks associated with tobacco.

4. Can I get life insurance if I have a pre-existing medical condition?

Yes, though premiums may be higher, and some conditions could lead to exclusions.

5. How does the type of policy affect my life insurance quote?

Term life policies usually have the lowest premiums, while whole and universal life policies cost more due to added benefits.

6. What happens if I provide inaccurate information on my application?

Misrepresentation can lead to denial of claims or cancellation of your policy.

7. Is it better to buy life insurance when you’re young?

Generally, yes, because premiums are lower and you lock in coverage before potential health issues arise.